Banks are scaling AI across customer support, profiling and personalisation, internal process optimisation, and credit-related workflows. EBA also highlights these as common application areas in EU banking and payments, signalling a shift towards repeatable solutions that can be embedded into day-to-day operations rather than one-off pilots.

This article outlines the AI banking solutions, the priority use cases, and the foundations required to scale well across the bank, followed by the five building blocks required to run them securely and consistently in production.

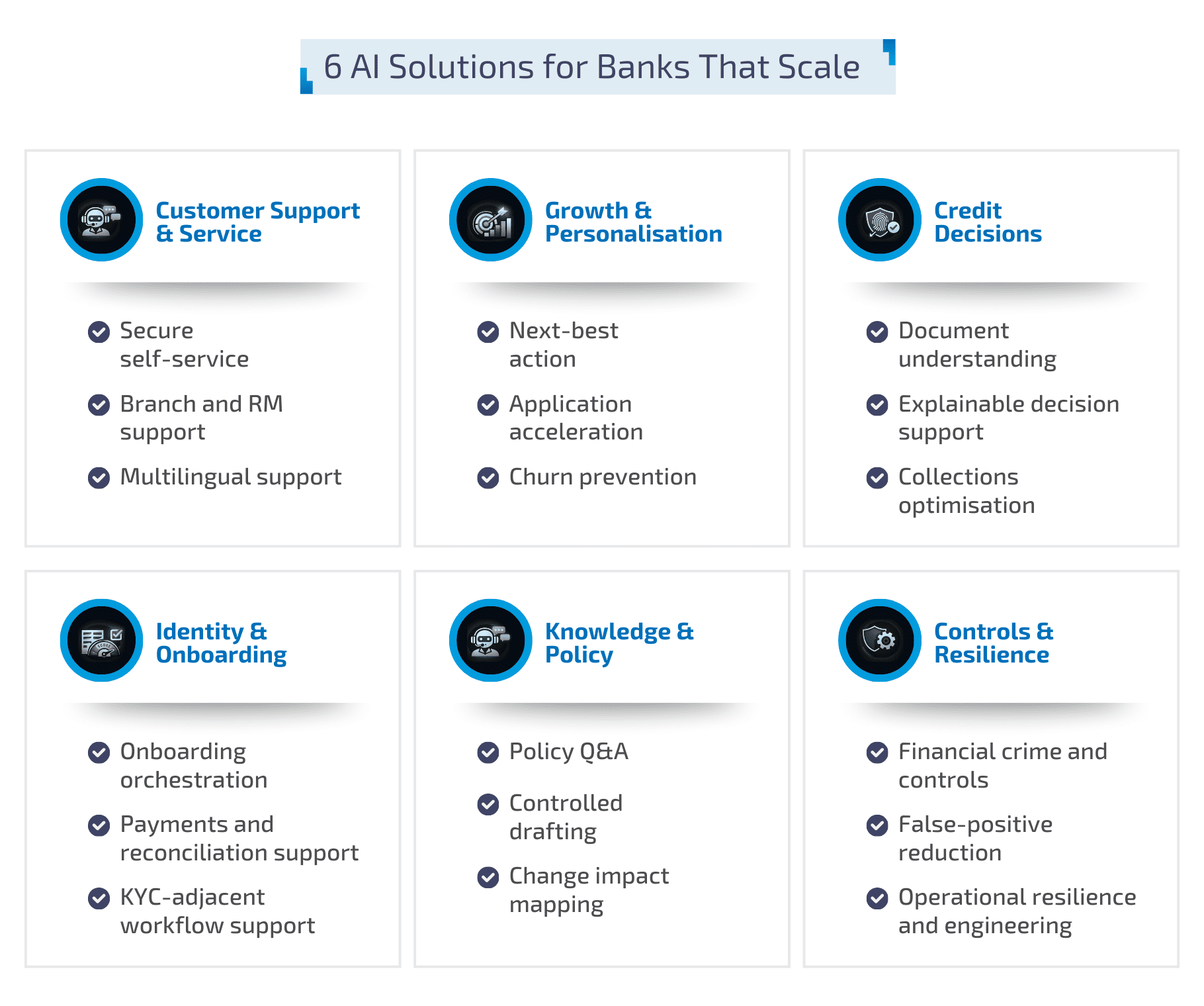

6 AI Solutions for Banks: Use Cases That Scale

In banking, “AI solutions” are not a single category. They typically fall into distinct solution families, based on where they sit in the customer journey, how decisions are made, and how much control and auditability is required. The strongest programmes treat these as repeatable building blocks that can be rolled out across products, teams, and countries, rather than one-off pilots.

1. Customer-facing and assisted service

- Secure self-service: Conversational self-service for routine requests, with safe escalation to human agents

- Branch and RM support: Agent-assist for contact centres and frontline teams, including summaries, guidance, and next-best response prompts

- Multilingual support: Consistent service quality across languages and channels

2. Sales, growth, and personalisation

- Next-best action: Recommendations based on customer behaviour, context, and eligibility rules

- Application acceleration: Pre-checks that flag missing information early and reduce drop-off

- Churn prevention: Early signals that trigger proactive outreach and retention actions

3. Credit, underwriting, and collections decision support

- Document understanding: Income and affordability checks using structured and unstructured documents

- Explainable decision support: Clear factors and evidence behind recommendations, aligned to policy

- Collections optimisation: Risk-led segmentation and timing to improve recovery and customer outcomes

4. Identity, verification, and onboarding automation

- Onboarding orchestration: Track documents, flag gaps, and trigger next steps across systems

- Payments and reconciliation support: Identify exceptions and suggest actions for operations teams

- KYC-adjacent workflow support: Evidence tracking and structured handovers for regulated onboarding journeys

5. Knowledge, policy, and communications enablement

- Policy Q&A: Answers grounded in approved sources, with citations and version control

- Controlled drafting: Customer and internal communications with review and approval steps

- Change impact mapping: Translate regulatory updates into affected policies and procedures

6. Controls, resilience, and technology operations

- Financial crime and controls: Fraud detection, AML alert enrichment, and prioritisation

- False-positive reduction: Noise reduction without weakening control effectiveness

- Operational resilience and engineering: AIOps and incident support, engineering copilots within SDLC controls, and cybersecurity monitoring for phishing and access anomalies

These solution families are proven starting points, but they only scale when the delivery foundations are in place. The next section outlines 5 architecture layers that make AI banking solutions production-ready, secure, and repeatable across teams, channels, and countries.

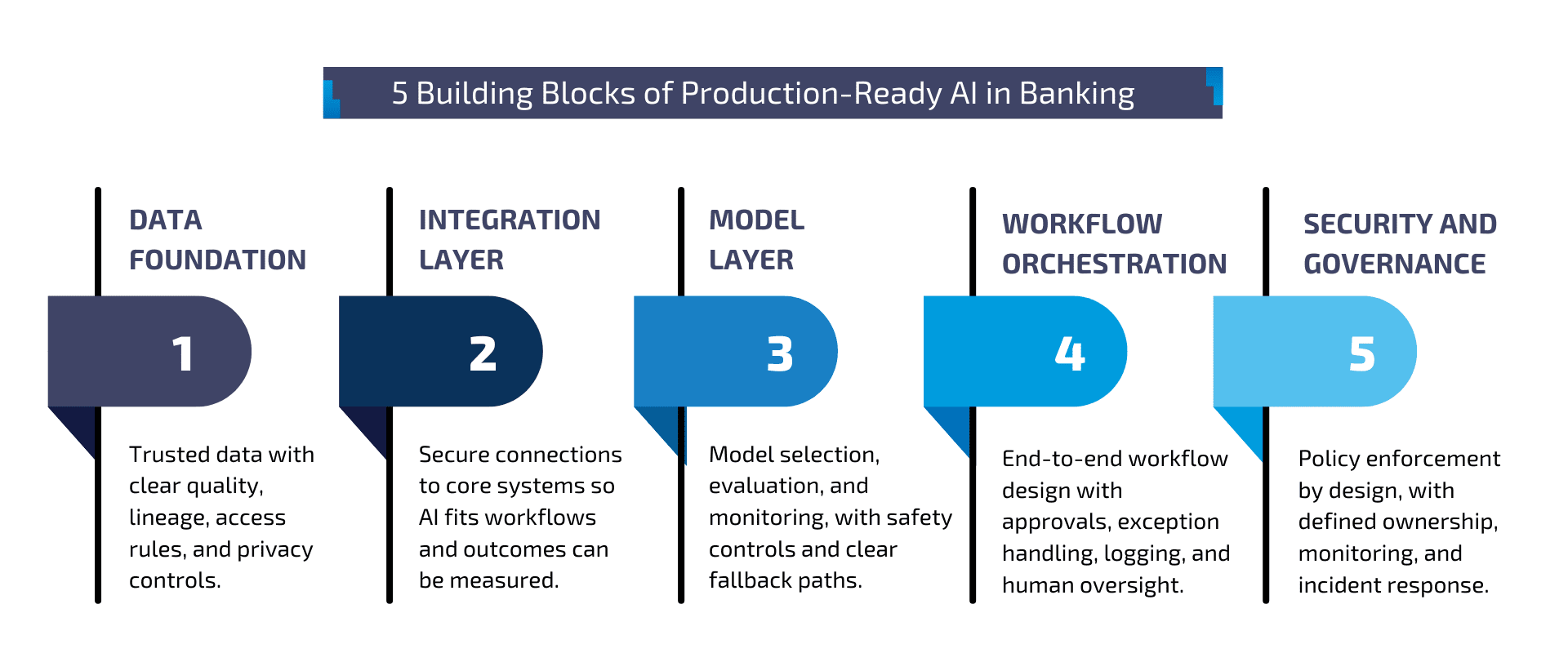

5 Building Blocks of Production-Ready AI in Banking

Scaling AI in banking depends on more than model capability. Banks are adopting AI at pace and these systems can operate with varying levels of autonomy, which increases the importance of strong foundations around data, integration, oversight, and governance.

5 Building Blocks of Production-Ready AI in Banking

1. Data foundation

AI is only as reliable as the data it uses. Banks need a clear view of data quality, lineage, access rules, and privacy constraints, with controls that ensure the right people and systems can use the right data for the right purpose. A practical approach is to start with a limited, well-governed dataset for each priority workflow, then expand coverage once monitoring and ownership are proven in production.

2. Integration layer

Most value comes when AI connects to core systems such as core banking, CRM, case management, KYC and AML tooling, and document repositories. Integration is also what enables traceability, operational adoption, and real performance measurement. Many programmes stall here. The bottleneck is rarely model capability. It is usually workflow fit, permissions, and the effort required to integrate AI into real operational pathways.

3. Model layer

The model layer includes model selection, evaluation, safety controls, and monitoring for drift and performance degradation. Banks benefit from a model strategy that supports different workloads, including predictive models and generative models, without assuming one approach fits all. Clear fallback paths matter. When confidence is low or data is missing, the system should route to a human, request clarification, or default to policy-safe outcomes.

4. Workflow orchestration

Orchestration turns AI into a solution rather than a feature. It defines how tasks move across systems, where approvals happen, how exceptions are handled, and what is logged for audit and control. Human-in-the-loop design should be intentional. It is not a last-minute add-on. It defines accountability, decision quality, and operational trust.

5. Security and governance

Scalable AI in banking requires policy enforcement by design: role-based access control, segregation of duties, data minimisation, logging, and monitoring. FSB highlights the importance of managing AI-related vulnerabilities, including third-party dependencies, as adoption increases.

AI governance also includes defined owners, approval paths, and incident response. These controls should be built into the workflow. The goal is to make compliance operational, not procedural.

Governance that stands up to audit

Audit-ready AI solutions require more than policy statements. Banks need governance that makes it clear what the system does, what data it relies on, how outcomes are produced, and who remains accountable when AI supports decisions that affect customers, capital, or controls. Documentation should be structured as an evidence pack for audit and risk review, covering purpose, scope, limitations, control points, monitoring, and operational procedures, alongside clear escalation and incident handling paths.

A useful framing is AIGA’s Hourglass Model, which links external requirements to organisational decision-making and, ultimately, to operational controls at the AI system level.

In practice, governance should define named owners for each use case and model, approval paths for changes, and ongoing monitoring for performance drift, data issues, and control effectiveness. Third-party risk also needs explicit oversight, including model providers, vendors, and data processors, with clear change management, access controls, and responsibilities for incidents and remediation. Where generative or agentic capabilities are used, audit readiness depends on traceability, logging, and a clear record of what was suggested, what was approved, and what was executed.

What to look for in an AI delivery partner

In banking, an AI delivery partner should prove they can operate in a regulated environment, not just build impressive prototypes. Look for a team with a track record of predictable delivery under governance, audit expectations, and operational resilience requirements, with clear change control and accountability. Security and data protection should be designed in from day one, including least-privilege access, strict data boundaries, redaction where needed, and secure integration patterns so the programme does not stall when it nears production.

You should also expect a mature governance and model risk approach: controlled outputs, robust evaluation, monitoring for drift, and documentation that risk and compliance teams can stand behind, with those stakeholders embedded throughout delivery rather than acting as a final gate. Finally, prioritise partners who can integrate AI into real banking workflows and measure outcomes with KPI discipline, delivering “answer plus action” across systems like case management, CRM, onboarding, or fraud operations, and tying success to metrics such as time-to-resolution, first-contact resolution, handle time, repeat contacts, and cost-to-serve.

How BGTS helps you operationalise AI banking solutions

At BGTS, we help banks take AI from priority use cases to production-ready delivery through end-to-end capability. Our services span strategy and roadmap, data engineering and readiness, integration and modernisation, generative AI enablement, and AI agents, alongside custom applications and analytics where needed.

Our work is strengthened by partnerships with leading technology providers including Temenos, Microsoft, AWS, ServiceNow, Atlassian, enabling secure integration into real banking environments. We also operate with a strong compliance baseline, backed by ISO certifications and Cyber Essentials Plus, so AI solutions are delivered with security, governance, and operational reliability built in.

Explore BGTS AI services or get in touch today to align on your priority use cases, operating model, and a practical delivery roadmap.